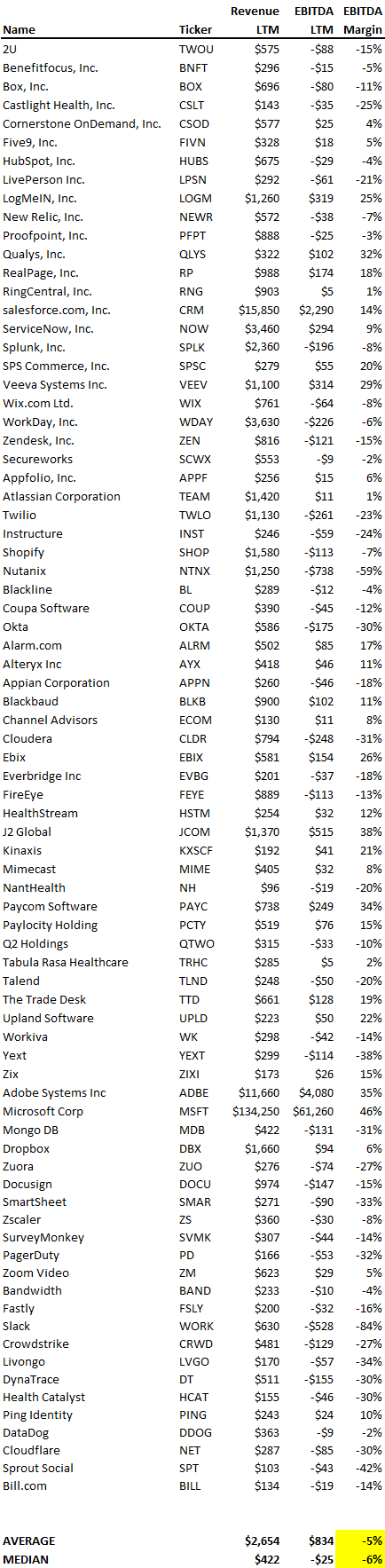

It’s common to hear “SaaS has great margins,” but that’s just not true. The margins in SaaS are terrible as the data below show. The table has 81 publicly traded SaaS companies with median revenue of $422mm meaning they’re well past the startup stage and margins should benefit from their scale and maturity. However, even though they’re past the high burn growth stage, the median EBITDA margin is -5% as 47 of the 81 companies are not EBITDA positive.

\

Why are these companies burning cash? Because while the variable costs of SaaS are very low (hosting, servers, etc), the fixed costs are very high, especially for engineering talent and developers. Given the speed at which technology becomes obsolete, the hiring of engineering/dev talent never really ends as each company has to constantly improve and evolve its product. Even worse, the fixed costs are all human talent, making it really painful to cut to morale, culture, and productivity of other personnel.

So why does SaaS work? Because traditionally SaaS companies collect their bookings up front. In other words, if you sell a 1 year contract for your software, the norm is to collect the cash up front for all 12 months as opposed to collecting 1/12th of the contract each month. It’s the reason that even though 47 of the 81 companies are EBITDA negative, only 25 of the 81 are cash flow negative. While the median EBITDA of the data set is -$25mm, the median cash flow is +$45mm. While cash flow is far better than EBITDA, it doesn’t change the fact that SaaS indeed has terrible margins.

Visit us at blossomstreetventures.com and email us directly with Series A or B opportunities at . Connect on LI as well. We invest $1mm to $1.5mm in growth rounds, inside rounds, small rounds, cap table restructurings, note clean outs, and other ‘special situations’ all over the US & Canada.

\

\