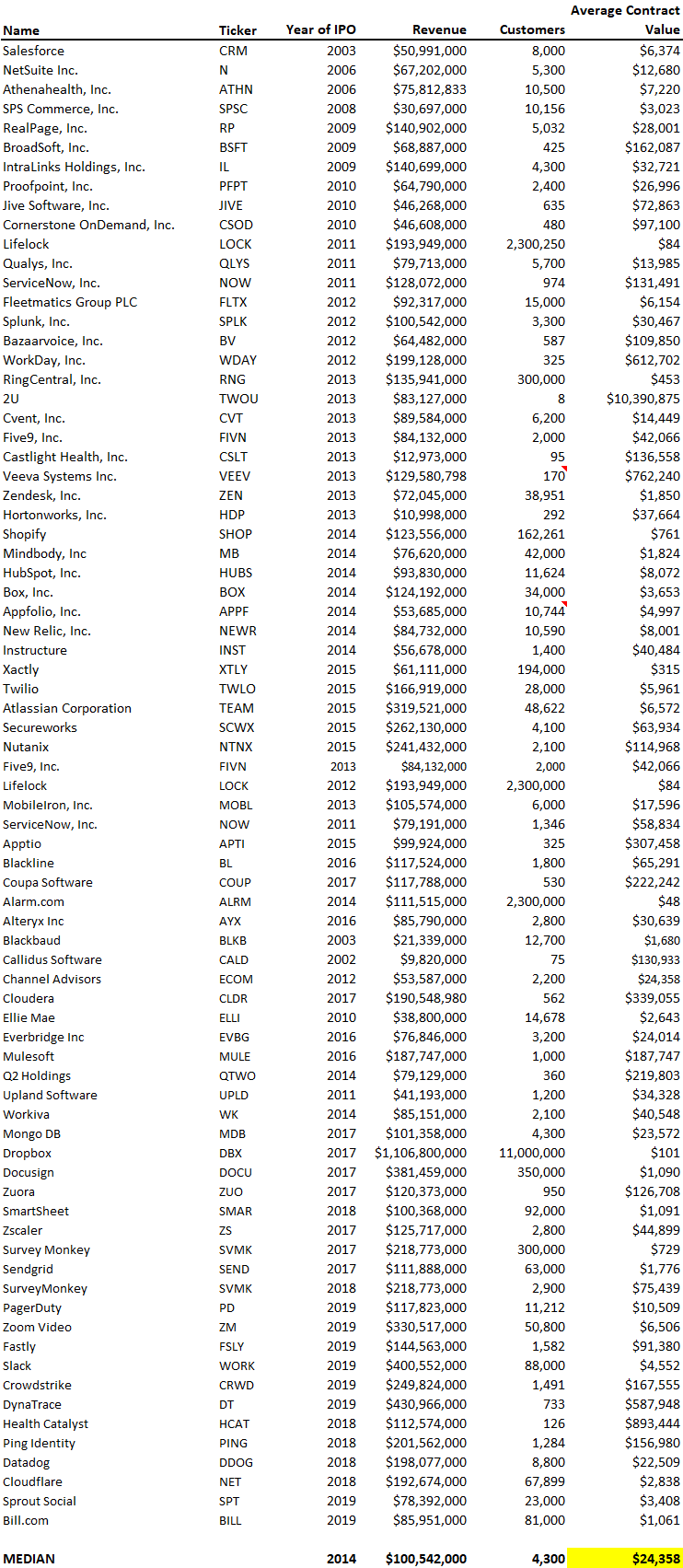

Average Contract Value is important, but don’t obsess over it. Maximizing ACV shouldn’t be the goal and as you’ll see below, SaaS companies that do IPO had a modest median ACV of $24k. A few observations:

Bigger software companies have smaller ACV’s. Below is a data set of 77 publicly traded SaaS companies and their estimated ACV’s when they went public. To do the analysis, we looked at each companies’ annual revenue relative to the number of customers prior to IPO (all contained in a filing called an S1). Upon going public, the median ACV was only $24,358. This makes sense as the universe of clients that can afford a lower ACV is much higher than those that can afford a $50,000+ ACV; by focusing on a lower ACV, you’ll be going after a larger market and have the opportunity to be a bigger, IPO worthy company.

Increases in ACV aren’t free. In order to increase ACV, it means some other metric of importance gets worse; for instance, the sales cycle gets longer, the close ratio comes down, and the number of leads needed to complete a sale increases. In order to achieve higher ACV’s, you have to focus on larger clients meaning more layers of management to achieve an approval, more time required to identify the decision maker, and more bureaucracy. It’s not uncommon to see sales cycles of 4 to 6 months for ACV’s over $20k and 6 to 9 months when ACV’s get to $50k+

ACV is a metric that should be monitored, but don’t change the way you sell in order to artificially increase it. While metrics like ACV are valuable, the real metrics you should be focused on are revenue and cash flow; ACV is only one of many ways to impact both.

Visit us at blossomstreetventures.com and email us directly with Series A or B opportunities at. Connect on LI as well. We invest $1mm to $1.5mm in growth rounds, inside rounds, small rounds, cap table restructurings, note clean outs, and other ‘special situations’ all over the US & Canada.