You probably won’t be a success from day 1. You’re going to struggle and may even come close to failure (more than once). The good news: there are plenty of examples of companies that had setbacks and bumps along the way, but were still a great success. Docusign is one such success story.

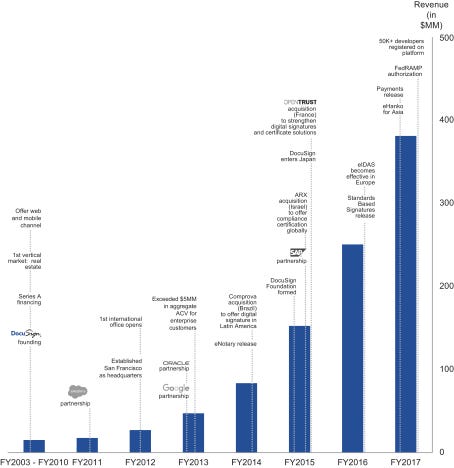

Docusign went public in 2018 with $381mm of total revenue and 350,000 total customers. While Docusign is a success, they’re also proof that the ride to success can be long and bumpy. Below is a graphic taken from Docusign’s public filings which shows what I’m talking about.

A few things stand out.

Docusign muddled along for years. Founded in 2003, the graph shows that by 2010 the Company had what looks like less than $10mm of revenue by that 7th year. Furthermore there was almost no growth in revenue from 2010 to 2011. The real growth didn’t actually start until 2013 when pivotal events were partnerships with Google and Oracle. That’s a full 10 years after founding.

The exit took 15 years. That’s well beyond the expectation of any angel investor and probably not what the founders had in mind. A successful exit was ultimately achieved, but the timeline was probably longer than anyone expected.

They burned through $650mm. That’s an extraordinary amount of capital for a software business. For comparison, we find that the median amount of equity and debt publicly traded SaaS companies have gone through before going public is well under $200mm.

Docusign was still not profitable. Operating loss in 2016 and 2017 was $119mm and $116mm respectively. Free cash flow was -$96mm and -$48mm in those years respectively.

Docusign went through a few CEO’s. The CEO at the time of going public, Daniel Springer, became CEO in 2017. From 2011 to January 2017 the CEO was Keith Krach. It’s unclear who the CEO was prior to 2011. The founder, Thomas Gonser, serves on the board. While it’s not uncommon for the founder to be replaced when a company transitions from startup stage to hundreds of millions of revenue, there are plenty of examples of tech companies where the founder is still the CEO (Salesforce, Snapchat, Facebook, Dropbox, Box, etc) and obviously you don’t change CEO’s unless there is a problem.

The learnings from Docusign are that not all successful startups look successful right away, there may be periods when growth is flat or slow, and the time and capital required may be more than anyone expects. Persevere.

Visit us at blossomstreetventures.com and email us directly with Series A or B opportunities at. Connect on LI as well. We like to lead or follow. We invest $1mm in growth rounds, inside rounds, small rounds, ‘tweeners’, cap table restructurings, note clean outs, and other ‘special situations’ all over the US & Canada.